Lowering the Medicare Age to 60: Cost and Coverage Outcomes

Executive Summary

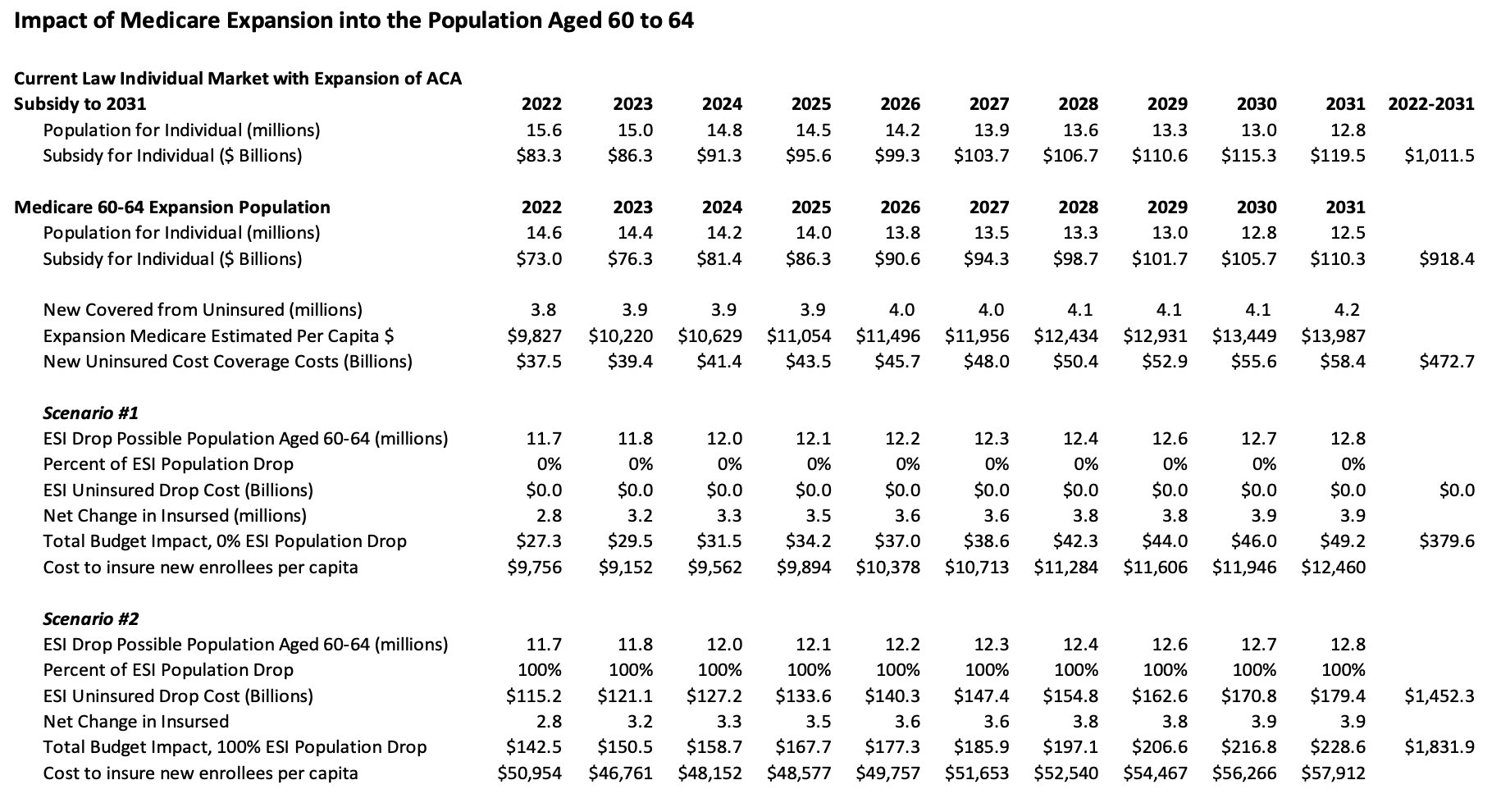

- Lowering Medicare eligibility to age 60 would cost $380 billion over 10 years—even after accounting for Affordable Care Act savings from lower spending on subsidies and assuming that employers continue to offer health insurance to those newly eligible for Medicare.

- If employers were to respond by dropping health coverage for employees age 60-64, the total cost of the policy would climb to as high as $1.8 trillion.

- Both scenarios would result in approximately 3.9 million additional insured individuals, at a cost of $9,756 to $57,912 per newly covered person.

Introduction

Last week congressional Democrats once again proposed lowering the Medicare eligibility age from 65 to 60, this time as part of the $3.5 trillion spending package they’re hoping to enact through the budget reconciliation process. The proposal was not ultimately included in legislative text released late last week—and even if had been included, past Senate precedent indicates it may not have complied with the rules of reconciliation.

Regardless of whether the eventual reconciliation package lowers the Medicare eligibility age, however, President Biden and congressional Democrats have made clear that doing so remains a policy priority, whatever the ultimate vehicle. New modeling from the American Action Forum’s Center for Health and Economy (H&E) shows that if Medicare eligibility were extended to those age 60-64, the cost to the federal taxpayer would be between $379.6 billion and $1.8 trillion over 10 years—depending on employer behavior in response to the change—and approximately 3.9 million more Americans would be insured (relative to H&E’s baseline estimates).

Scenarios and Assumptions

H&E modeled two scenarios (as shown in Table 1) for lowering the Medicare eligibility age resulting in a lower and upper bound for cost to the federal government.

Scenario 1 assumes that all employers continue to offer employer-sponsored insurance (ESI) to the newly Medicare-eligible population and that those age 60-64 are able to choose between ESI and Medicare, resulting on $380 billion in new federal spending.

Scenario 2 assumes that 100 percent of employers stop ESI coverage for those age 60-64, leading to a complete migration of that age cohort into Medicare and resulting in new federal spending of $1.8 trillion.

Both scenarios assume that those age 60-64 who are currently covered by Medicaid would remain in Medicaid coverage, and that all currently uninsured individuals age 60-64 enroll in Medicare. Cost estimates for both scenarios are net savings derived from lower federal spending on premium tax credits through the Affordable Care Act (ACA) marketplace. H&E estimated the per capita cost of expanded Medicare at roughly equivalent to that of unsubsidized premiums for a Silver plan in the individual market for the age 60-64 cohort.

H&E projects that both scenarios result in a net increase of approximately 3.9 million in the total number of insured Americans, relative to the H&E baseline. That coverage expansion would come at a cost of between $9,756 to $57,912 per newly covered individual, depending on year and share of the ESI population enrolled in the expansion.

Table 1.

Conclusion

Policymakers could structure a Medicare expansion in a number of ways to attempt to minimize the scorable cost of the policy. Based on H&E estimates, however, a straightforward expansion of Medicare down to age 60 would result in a substantial increase in federal spending—between $380 billion and a $1.8 trillion over 10 years or between $9,756 to $57,912 per newly covered individual, depending on year and share of the ESI population enrolled in the expansion. Medicare expansion has become an ideological litmus test for progressives, but for a purely dollars-and-cents perspective, extending Medicare coverage to those age 60-64 is a case where the benefits are unlikely to outweigh the costs.